The Prime Minister Youth Loan Scheme 2026 stands as a cornerstone of the Pakistani government’s strategy to uplift the nation’s youth. By providing accessible capital with highly subsidized markup rates, the program enables aspiring business owners to turn their visions into reality. This initiative is more than just a financial tool; it is a strategic effort to stimulate the national economy, spark creative entrepreneurship, and create sustainable jobs.

Below, we break down everything you need to know to navigate the application process and maximize your chances of success.

Requirements for the PM Youth Business Initiative

To ensure that funds are distributed effectively to the most promising candidates, the government has established specific eligibility benchmarks. Meeting these criteria is the first step toward securing financial backing for your venture.

Age Requirements

The program is tailored to different sectors, offering more flexibility to the digital economy:

- Standard Ventures: Applicants should be between 21 and 45 years of age.

- Tech & Digital Trade: For those launching IT or e-commerce startups, the minimum age requirement is lowered to 18 years.

Citizenship & Identity

This initiative is exclusively for Pakistani nationals. Every applicant must possess a current and valid Computerized National Identity Card (CNIC) to prove their status and residency.

Business Strategy

A viable business roadmap is a critical component of the selection process. You must present a practical plan that outlines your goals, target market, and projected revenue. A high-quality, realistic strategy significantly boosts your likelihood of being shortlisted.

Skill set and Background

While the scheme is open to all, your profile will be viewed more favorably if you possess:

Relevant academic degrees or certifications.

Prior work experience in your chosen industry.

Technical training or vocational certificates.

Overview of the Youth Loan Scheme 2026

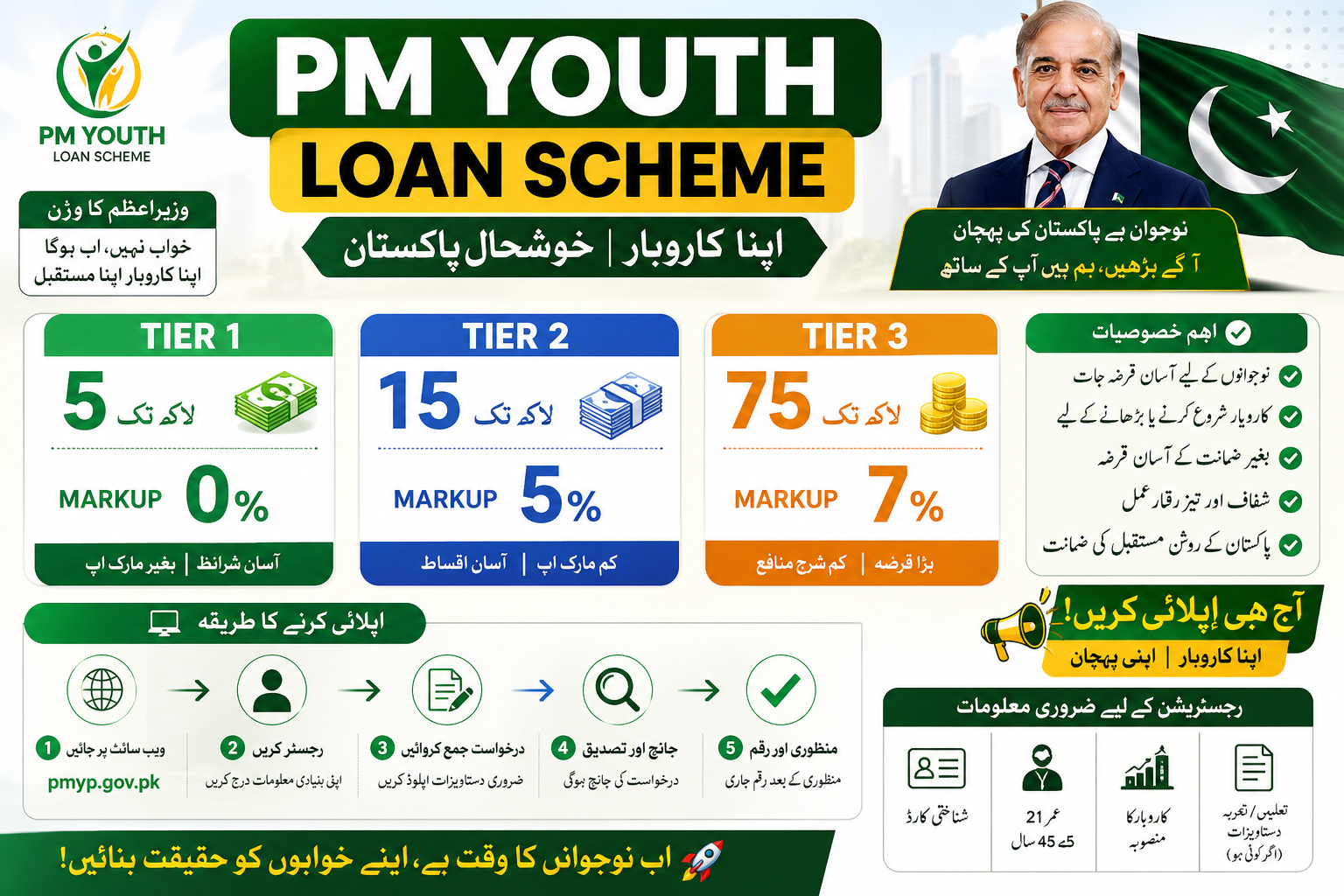

The Prime Minister Youth Business & Agriculture Loan Scheme (PMYB&ALS) is designed to provide accessible financial support to the next generation of Pakistani leaders. Below is a snapshot of the key program features and the tiered financing structure.

Tier 1: Small Scale & Micro-Ventures

Loan Range: Up to PKR 500,000

Markup Rate: 0% (Interest-Free)

Collateral: Based on a personal guarantee.

Tier 2: Mid-Level Business Growth

Loan Range: Above PKR 0.5 Million to PKR 1.5 Million

Markup Rate: 5% Fixed

Focus: Perfect for expanding existing setups or more robust startups.

Tier 3: Large Scale Entrepreneurship

Loan Range: Above PKR 1.5 Million up to PKR 7.5 Million

Markup Rate: 7% Fixed

Requirement: Security/Collateral as per the participating bank’s specific credit policy.

Application Roadmap: Securing Your Business Funding

Navigating the application process for the PM Youth Business & Agriculture Loan Scheme is straightforward if you follow these systematic steps. Ensure you have a stable internet connection and all your digital documents ready before beginning.

Phase 1: Accessing the Digital Gateway

Start by navigating to the official PMYB&ALS web portal. This is the only legitimate platform for submissions. Be cautious of unofficial websites or social media links that ask for personal data outside of this government-secured domain.

Phase 2: Completing the Digital Registration

Once on the portal, you will be required to fill out a comprehensive electronic form. Accuracy is vital here. You will need to provide:

- Identity Details: Full legal name, CNIC number, and family background as per NADRA records.

- Contact Information: Active mobile number and mailing address.

- Project Profile: A clear description of your business concept, including your objectives and how the funds will be utilized.

Phase 3: Document Uploads

To validate your request, you must attach digital copies of your credentials. At a minimum, have the following ready:

- A scanned, clear copy of your Identity Card (CNIC).

- A formal Business Feasibility Study (this document is the core of your application).

- Any optional supporting files, such as diplomas, trade licenses, or experience letters, which can bolster your credibility.

Phase 4: Final Verification and Submission

Before clicking the submit button, perform a final audit of your entries. Small errors in your phone number or CNIC can lead to delays or automatic rejection. Once you are confident the data is correct, finalize the submission.

Phase 5: Tracking Your Progress

Upon successful submission, the system will generate a unique tracking ID or reference number. Save this number securely. You can use it on the portal’s “Track Application” page to monitor the status of your loan request as it moves through the bank’s verification and approval stages.

Pro Tip: Keep your mobile phone active and reachable. Bank representatives often conduct telephonic interviews or physical site visits as part of the final verification process.

Partner Financial Institutions

The following banks are authorized to manage and process loan applications for this initiative:

- National Bank of Pakistan (NBP)

- Bank of Punjab (BOP)

- Meezan Bank

- Habib Bank Limited (HBL)

- Bank Alfalah

Prospective borrowers are free to choose the institution that aligns most closely with their personal requirements and location.

Tips for a Successful Application

To maximize your chances of approval, steer clear of these frequent pitfalls:

Gaps in Information: Double-check that every field in your application is completed correctly. Providing partial details is a common reason for immediate disqualification.

Vague Business Proposals: A weak or unrealistic plan can hurt your credibility. Take the time to develop a strategy that is specific, data-driven, and clearly outlines your path to success.

Omitted Documentation: Before submitting, verify that all essential attachments such as your CNIC, comprehensive business plan, and relevant certifications are included.

Taking a proactive approach to these details will significantly strengthen your submission and boost your likelihood of success.

Frequently Asked Questions

1. Who is eligible to submit an application? Citizens of Pakistan between the ages of 21 and 45 who possess a valid Computerized National Identity Card and a practical business strategy may apply. For those in the Information Technology or digital commerce sectors, the minimum age requirement is lowered to 18 years.

2. What is the maximum financing available? Under the third category of this initiative, applicants can secure a maximum of 7.5 million Pakistani Rupees.

3. What steps are involved in the submission process? Prospective borrowers must utilize the authorized web portal to complete their registration. The process involves filling out the digital application and attaching all necessary supporting files.

4. Which records must be provided? You will need to provide your valid identification card, a detailed professional roadmap for your business, any applicable academic or skill-based credentials, and a current passport-sized photo.

5. Is security or a guarantee required? The necessity for providing collateral varies based on the total funding requested and the specific internal regulations of the chosen financial institution.

Final Summary

The Prime Minister’s Youth Business and Agriculture Loan Scheme (PMYB&ALS) serves as a pivotal catalyst for Pakistan’s economic growth. By offering accessible financing including interest-free loans up to Rs 0.5 million it enables aspiring entrepreneurs and farmers to actualize their professional goals. Whether launching a tech startup or expanding agricultural operations, this initiative provides the essential capital and favorable terms required to drive national innovation and self-sufficiency through 2026.